|

Reading a credit report

You will need to adapt the information covered on this page

depending on the level of your students. If your students

are at a beginning level, you may

want to leave out a discussion of some of the finer points

of reading credit information. If your students are at a

higher level, you may want to obtain different kinds of

sample credit reports from credit reporting agencies and

compare how the information is presented in each report.

For beginning-level students

Review the concepts found in the identification, residence,

and employment sections of the report. These concepts include

writing one’s name, address, phone number, Social Security

number, and number of dependents; and reading and writing

dates and job titles.

For more advanced students

Practice reading each column of the credit history section

of the report, explaining such concepts as date

opened, credit limit, balance, amount past due, past due

records, and

revolving credit.

Mention that credit reports sometimes report incorrect

information. For this reason, it is a good idea to get a

copy

of your credit report and check it for accuracy before applying

for credit.

Going further

Invite a representative from a credit reporting agency or

nonprofit credit counseling service to speak with students

about credit reports and

establishing good credit habits.

Comprehension check

Have students work in pairs or small groups to locate the

answers. For more practice, have students use the sample

form to make up additional questions for their classmates

to answer.

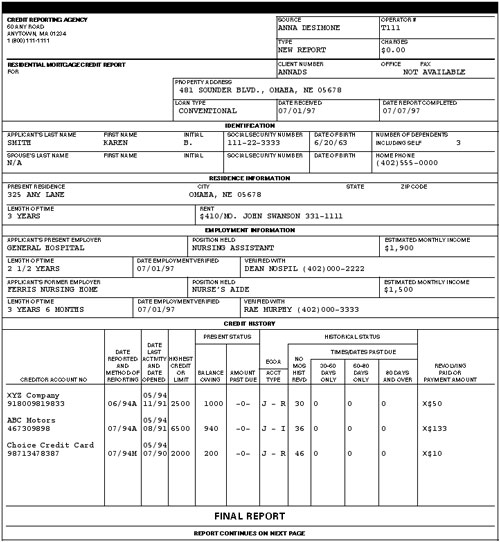

Talk about it

You may want to spend some time discussing Karen Smith’s

credit history. Point out that Karen Smith appears to pay

her bills on time. She has no late bills at this time. The

lender should

see her as a good credit risk.

Point out that if Karen Smith were married, she might be

applying for a loan as a co-borrower, and the credit record

of both partners would be checked. It is important for each

partner in a marriage to establish his or her own credit

so that if he or she becomes divorced or widowed, he or

she will have a credit record of his or her own, as Karen

does.

Going further

Every credit reporting agency may present its information

a little differently. If you can, get a copy of one or two

additional sample credit reports from agencies. You may

be asked to “white out” some of the personal information

for privacy

reasons and look only at the credit history portion of the

form.

|